Knowledge Centre

Commodities Bottom Out

July 2017

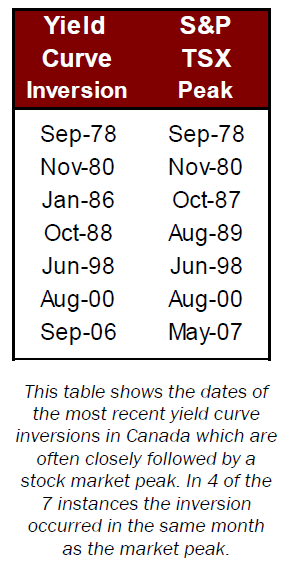

Typically, commodity prices go through longer bear market cycles compared to bull market cycles while the opposite is usually true for stock prices. While Canadian equity markets are slightly off the record highs set in February 2017, commodities, relatively speaking, are dirt cheap. In fact, they are basically the cheapest they have been since the all-time high was reached in June 2008. Commodity prices have fallen 56.9%, based upon the decline in the S&P GSCI Commodity Index over the past 9 years.

This surprisingly repetitive pattern is starting to show that bargains in the commodity sector are present and many of the best Canadian resource stocks are at incredible discounts. In fact, commodity prices appear to be in the process of bottoming after trending lower during the last three years of this recovery following the OPEC decision in June 2014 to ratchet up oil production, which slashed prices. Given the potential of a hike in Canadian interest rates by the Bank of Canada (which appears to be just over the horizon) there may be an important shift in economic pricing power which has historically altered stock market leadership (i.e. commodities dictating the direction of the overall stock market).

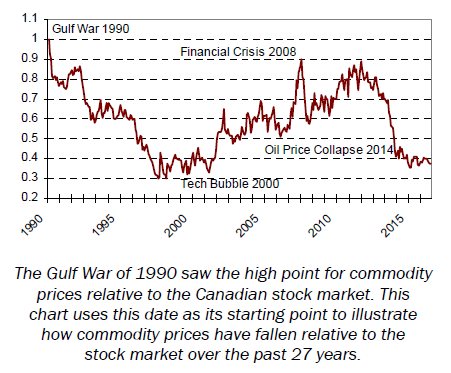

The ratio of the S&P GSCI Commodity Index (which is priced in US dollar terms) to the S&P TSX Canadian Stock Index, which has historically pin-pointed peaks and valleys in commodity prices, is now very close to its lowest levels since 1990. The Gulf War of 1990 represents the very peak of this ratio and was the high point for commodity prices relative to the Canadian stock market. The chart to the right uses this date as its starting point to effectively illustrate how low commodity prices have fallen relative to the stock market over the past 27 years.

A significant decline in commodity prices during an economic recovery is very common. During the late 1970s, 1980s and 1990s recoveries, commodity prices suffered severe falls. Those economic recoveries continued well after the bottom in commodity prices was reached and did not end until commodity prices had substantially recovered all their losses. The current malaise looks very similar to the tech bubble of 2000. This can mean three things: stocks are expensive; commodities are truly cheap; or the financial market is correctly factoring in economic growth which no longer relies on commodities (highly unlikely).

Looking down the road, the strong historic relationship between the Canadian dollar and the price of oil has recently de-coupled as the potential for an interest rate hike looms. It is this disconnect that is showing that although oil prices are still very weak, they have been in a bottoming process since early this year. As such, commodity markets could soon embark on a multi-year advance which will likely alter leadership in the economy and in the stock market.

A significant decline in commodity prices usually points to stronger, rather than weaker, future economic growth. Moreover, once commodity prices do finally bottom, they have typically risen throughout the balance of the economic recovery. Keep in mind that successful investing is a marathon, not a sprint.

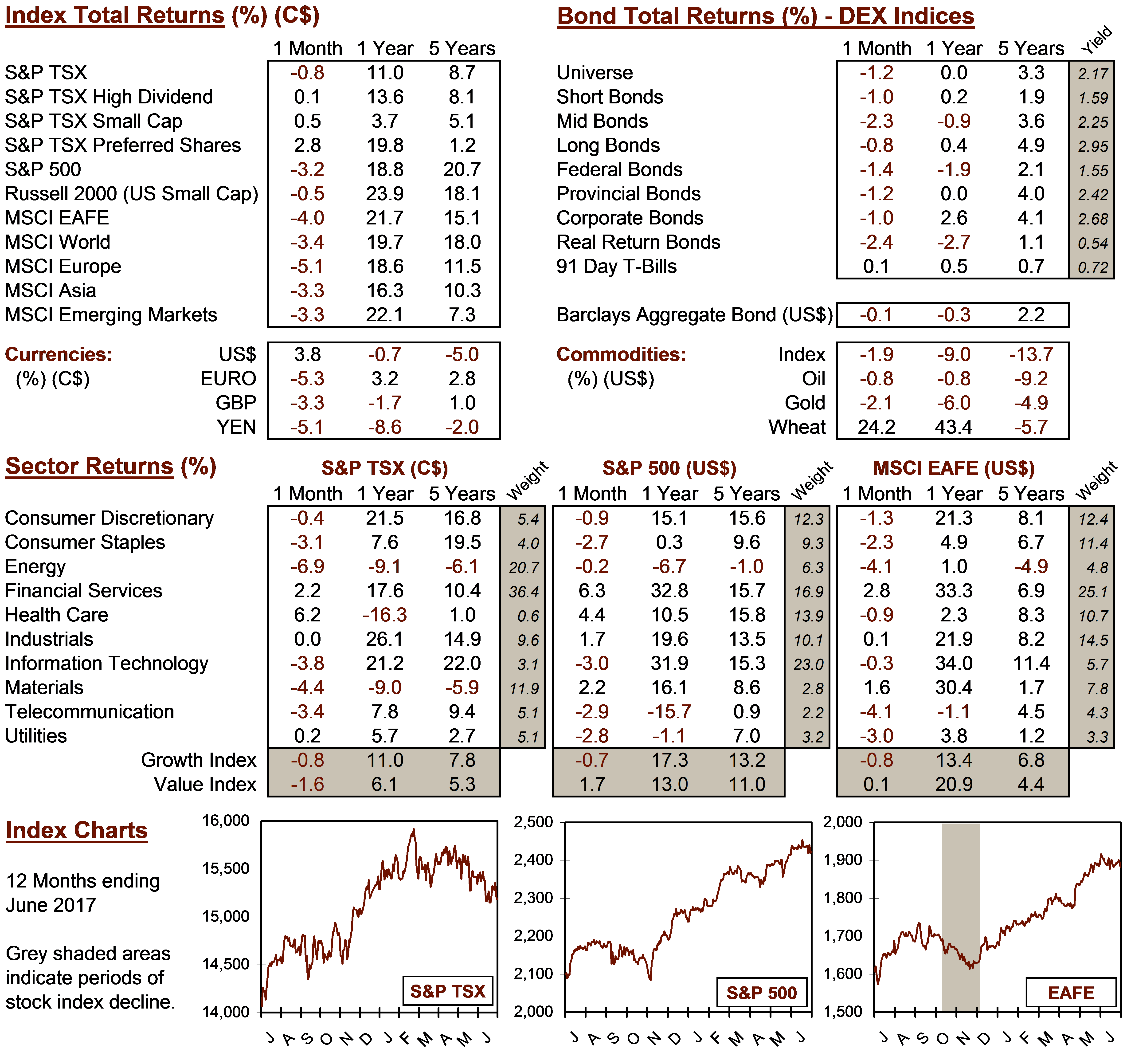

MARKET DATA

This report may contain forward looking statements. Forward looking statements are not guarantees of future performance as actual events and results could differ materially from those expressed or implied. The information in this publication does not constitute investment advice by Provisus Wealth Management Limited and is provided for informational purposes only and therefore is not an offer to buy or sell securities. Past performance may not be indicative of future results. While every effort has been made to ensure the correctness of the numbers and data presented, Provisus Wealth Management does not warrant the accuracy of the data in this publication. This publication is for informational purposes only.

Contact Us

18 King St. East Suite 303

Toronto, ON

M5C 1C4