Knowledge Centre

Range Bound No More

November 2017

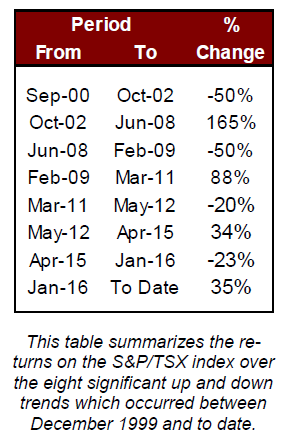

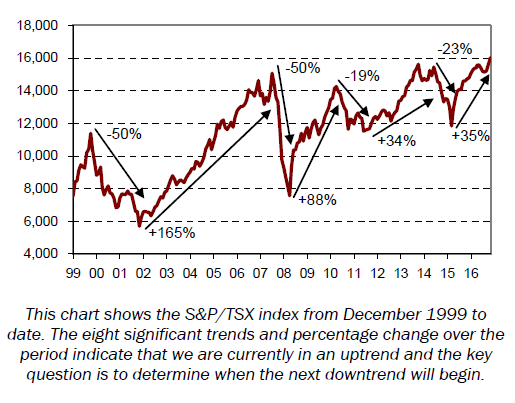

After every major bull market, stocks typically become range bound and experience a sideways pattern with many optimistic and pessimistic periods before exiting 15 to 30 years later at about where it began. This has occurred in the U.S. five distinct times since 1870: 1870 to 1900 (lasting 30 years); 1902 to 1927 (25 years); 1935 to 1950 (15 years); 1965 to 1980 (15 years) and of course the most recent starting in 2000. Although Canadian stock market history does not extend back quite so far the pattern is very much the same, which should be expected since we march to the same drummer. Ultimately, the advancing economic recovery results in enough earnings growth that stocks that once seemed expensive are now bargains, and triggers a new bull market when stocks break through the upper constraints of the range.

Back in 2008, following a robust record high equity bull market, investors were feeling optimistic. Not surprisingly the flows into equities were significant. This was when the current sideways market began with a bull market peak of 15,073 in June 2008 for the S&P/TSX index. Seven years later in April 2015, the market was barely higher at 15,451. The market continued to oscillate for the next two years, unable to climb above 15,500. However, this began to change over the last two months.

History is a reasonable guide for what might occur next and it has suggested a new bull market is fully established once the range is broken. Only those perceptive enough to see though the market "noise" will be rewarded by the time the new upward trend is well entrenched. And it appears the markets have now finally broken out of this range by firmly establishing new highs.

As is evident in the chart to the right and in the table to the left, the equity market's gyrations over the last 10 years have produced little tangible gains unless investors were astute enough to tactically determine the right time to buy and sell stocks. History suggests that investors with a long term horizon will achieve better returns in equities (probably 6% to 9% annualized) than in most other investments.

Investors have been pulling money out of equities and adopting bonds as the "must have" alternative, which was part of a broader trend that has been going on since the middle of the last decade. The financial crisis of 2008 made investors increasingly more risk averse and drove them to higher yielding investments as a way to maximize their returns in an era where longer term gains from the prices of stocks alone had proven elusive. With a record 21% of the workforce now aged over 55 and growing quickly, the asset mix of the general population is structurally biased towards instruments that generate an income stream as concerns over retirement percolate. This had put more pressure on stock valuations and dampened the desire for riskier assets.

Following extended periods of weakness, history shows that the future should be quite bright. After all of the worst performing 10 year periods since 1926, the following 10 year average returns were close to 11% and the lowest of those subsequent returns was still over 7%. Logic would dictate that investors should take profits in those asset classes that had performed the best, which in Canada were bonds and real estate, and seek returns in the weakest asset class, which has been equities. In the midst of the current equity rally, ten year government bonds are yielding less than 2% so a potential annualized return of 7% in equities over the next 10 years would be very attractive.

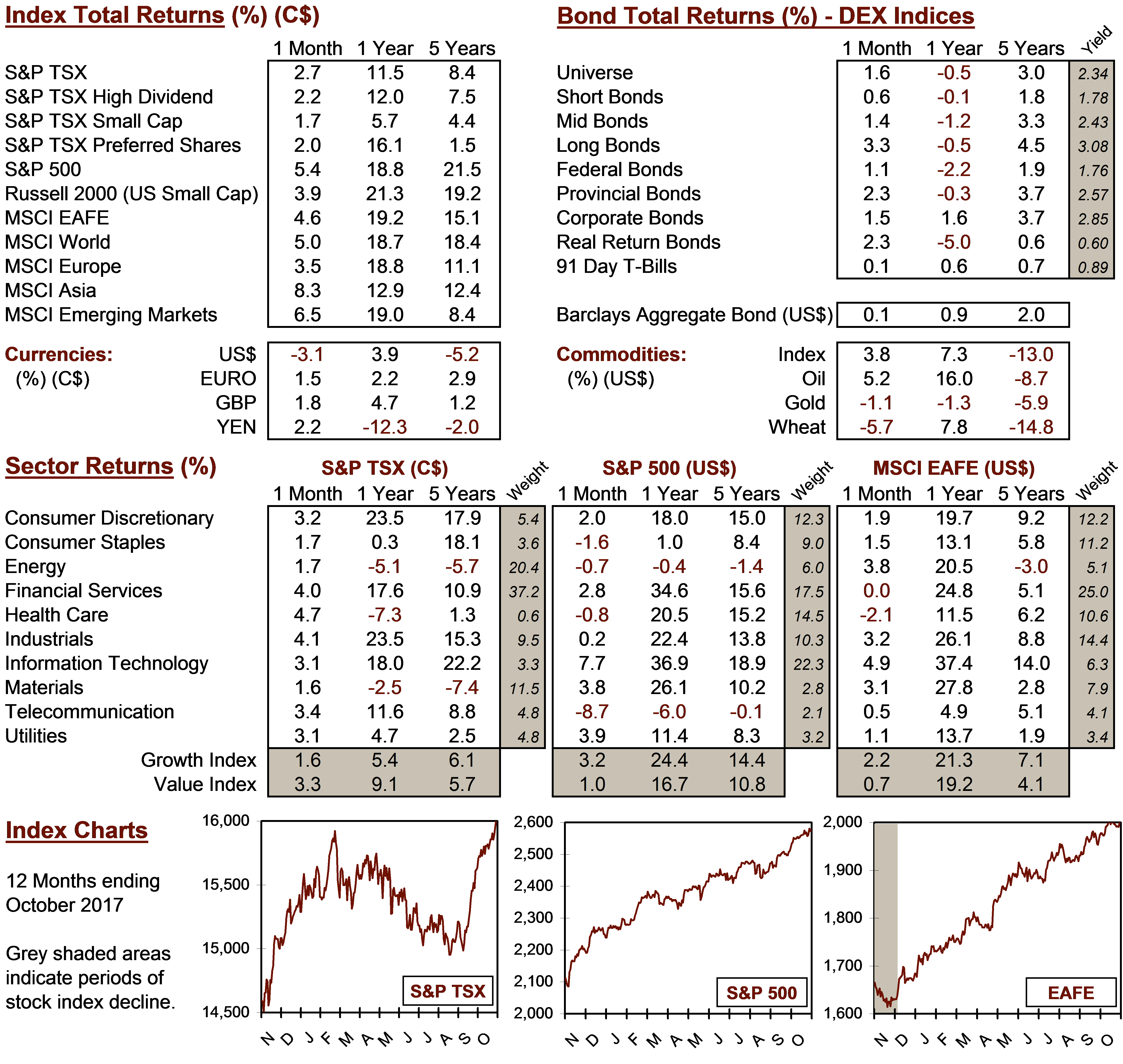

MARKET DATA

This report may contain forward looking statements. Forward looking statements are not guarantees of future performance as actual events and results could differ materially from those expressed or implied. The information in this publication does not constitute investment advice by Provisus Wealth Management Limited and is provided for informational purposes only and therefore is not an offer to buy or sell securities. Past performance may not be indicative of future results. While every effort has been made to ensure the correctness of the numbers and data presented, Provisus Wealth Management does not warrant the accuracy of the data in this publication. This publication is for informational purposes only.

Contact Us

18 King St. East Suite 303

Toronto, ON

M5C 1C4